Why the Shale Revolution Could Only Happen in America

A few weeks ago we wrote Why Oil Could Be Higher for Longer, and since then it has elicited quite a few comments back to us from clients and blog subscribers. We won’t repeat it in detail here since readers can simply click on the link above to see it. But our view is that the outlook for U.S. crude production over the intermediate term is very constructive, and certainly better than current consensus. This relates to the superior economics of shale wells compared to conventional drilling, and the associated ability of shale Exploration and Production (E&P) companies to quickly respond to changing prices by adjusting drilling activity faster than their peers.

“Shale wells,” (i.e horizontal wells drilled into source rock and stimulated by fracking) have many competitive advantages over conventional wells that give us confidence American production of Oil, Natural Gas Liquids (NGLs), and Natural Gas will greatly exceed consensus expectations to meet new energy demand and fill the void left by depleting fields.

A recent article in the Financial Times expanded on this theme (U.S. shale is lowest-cost oil prospect). A chart accompanying the article showed the break-evens of twenty potential future projects and the cheapest half-dozen are U.S. shale plays. In fact, shale oil development benefits from many of the advantages that are inherent in the U.S. Most Americans take for granted that property ownership comes with mineral rights for anything found below their property, but around the world this is by far the exception. In most countries mineral rights belong to the government. Getting a farmer to agree to allow drilling on his land is easier if he’s able to negotiate a monthly royalty check as opposed to a central authority simply exercising its control.

Although many of the cheaper sources of new oil are U.S. shale, Wood Mackenzie doesn’t believe there’s enough to satisfy the world’s consumption at current prices. Depletion of existing fields plus new demand create a need for roughly 6MMBD (million barrels a day) of additional supply annually. The market will clear at the marginal cost of the most expensive barrel needed to balance the market – a price that looks a good bit higher than today’s spot price. And for those who think offshore drilling can be attractive, BP just announced the final charge of $5.2BN for the 2010 Deepwater Horizon spill in the Gulf of Mexico. Their total costs for this one incident add up to $61.6BN, a hit only a few global companies could absorb. You can be sure that any offshore drilling in U.S. continental waters has to account for this possibility in its risk analysis.

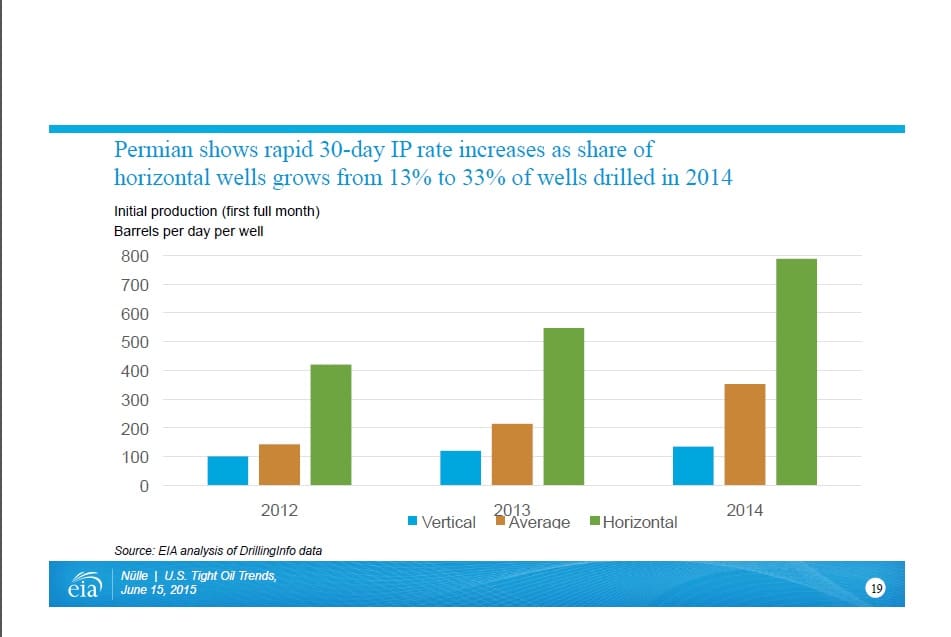

Critically, low-cost U.S shale wells can be drilled much more quickly and come on with significantly higher initial production (IP) rates with steep decline curves. In fact, a new shale well can go from planning to full capital payback before most new conventional projects are even producing. This fast decline rate also allows shale oil producers to hedge the bulk of their production, which occurs in the first several years, in the futures market which is only liquid for a few years out. It’s worth noting that the quicker the payback the quicker shale E&Ps can plowback cash into new shale drilling. The chart below from the U.S. Energy Information Agency highlights how IP rates have improved over the past few years (click on image to expand).

Geographically, the U.S. is blessed with generally sufficient water supplies close enough to the shale plays that they support, since fracking requires a lot of water. Entrepreneurial drive is as strong a force in America as anywhere, and that combined with highly developed capital markets make access to financing and substantial wealth accumulation possible for those who are able to profitably exploit this resource. And continued technological innovation spurred by entrepreneurs is relentlessly driving costs down faster than most expected and faster than conventional plays, further increasing their competitive cost advantages, playing to another American strength.

Even with all the American advantages and helped by the tailwind of high commodity prices it still took a decade for shale drilling to have a meaningful impact on output. Major shale drilling anywhere outside the U.S is a long way off, providing a huge first mover advantage.

In other words, the shale revolution is occurring because of all these inherent strengths in the U.S. On top of which, energy independence which is where we’re heading as a result, is in our national interest and highly likely to remain that way. The entire story is built on U.S. advantages and oriented towards U.S. interests. From a strategic perspective, given what we know today, it seems to us that perhaps the best secular investment theme available is the continuation of this trend, to the obvious benefit of the midstream infrastructure Master Limited Partnerships (MLPs) whose support is critical.

It’s no longer the case that a distribution cut is bad for an MLP. In April, Crestwood Equity Partners (CEQP) cut its distribution at the same time as announcing a JV with Con Edison and steps to reduce its leverage (see Crestwood Delevers and Soars). Last week Plains GP Holdings (PAGP) announced a simplified structure with its MLP Plains All America (PAA) and an 11% distribution cut at PAGP. Both stocks moved sharply higher on a perceived lower cost of capital and therefore improved growth prospects. Williams Companies (WMB) is likely to cut its dividend so as to reduce leverage, but at a 12% yield there can be few who would be surprised by this. A distribution cut in support of a stronger balance sheet seems to attract more buyers than sellers nowadays.

Lastly, we note that Shell Chemicals is investing $6BN in a new ethylene facility in SW Pennsylvania near Pittsburgh (artist’s impression from Shell at left). It’s located there to be close to its supply of ethane in the Marcellus and Utica shale areas, of which it expects to consume 90-100 thousand barrels a day. The facility will in turn produce 1.5 million tonnes per annum (MTPA) of ethylene and 1.6 MTPA of polyethylene, widely used in everything from food packaging to automotive components. This is not a region that has seen a new large industrial project such as this in living memory. It’s another example of the tangible results of the shale revolution.

Lastly, we note that Shell Chemicals is investing $6BN in a new ethylene facility in SW Pennsylvania near Pittsburgh (artist’s impression from Shell at left). It’s located there to be close to its supply of ethane in the Marcellus and Utica shale areas, of which it expects to consume 90-100 thousand barrels a day. The facility will in turn produce 1.5 million tonnes per annum (MTPA) of ethylene and 1.6 MTPA of polyethylene, widely used in everything from food packaging to automotive components. This is not a region that has seen a new large industrial project such as this in living memory. It’s another example of the tangible results of the shale revolution.

We are invested in CEQP, PAGP and WMB

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Two quick points about the article.One, the shale characteristics described in the article should benefit not only oil-based MLPs but also those dealing with associated gas from those,wells. And two, unfortunately the Shell Pennsylvania facility referred to is years away, probably a 2020 project.