NuStar Acts Like a Hedge Fund

Last Tuesday, in a kind of return to normalcy, NuStar Energy (NS) funded an acquisition the way Master Limited Partnerships (MLPs) normally do; by issuing equity.

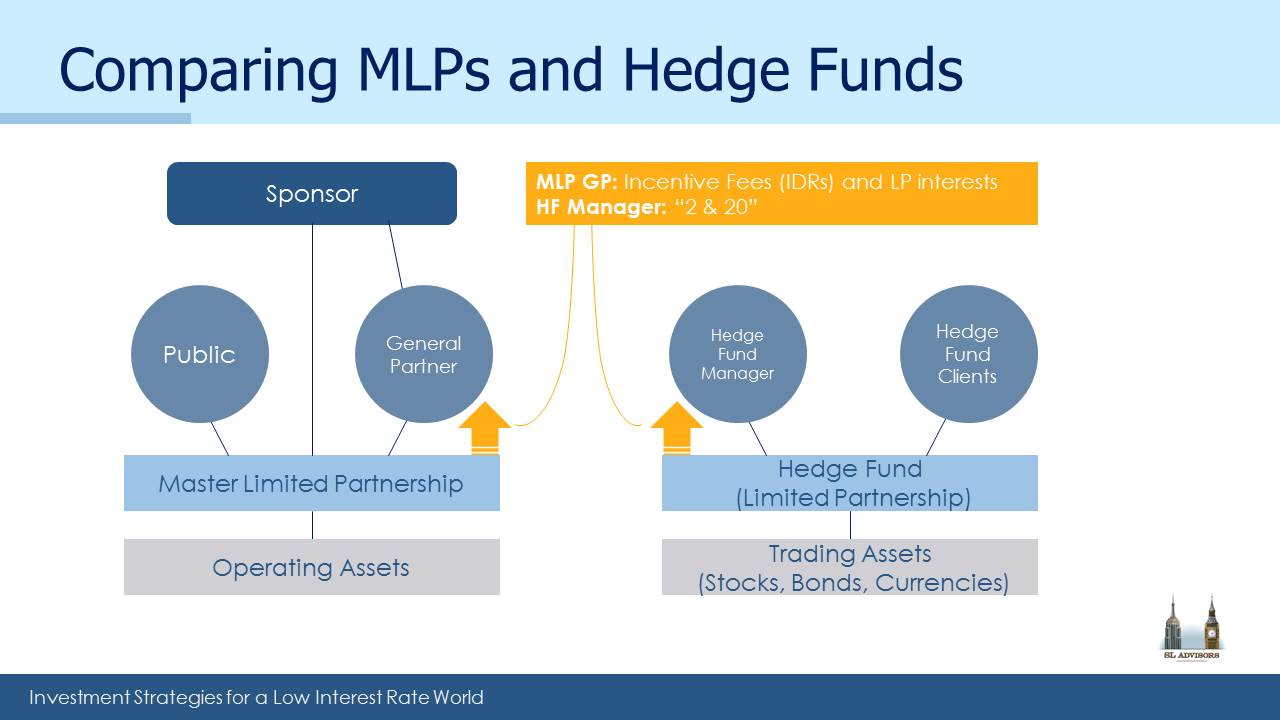

NS is an MLP controlled by a publicly traded General Partner (GP) called NuStar GP Holdings (NSH). As we’ve noted in the past, an MLP with a GP looks very like a hedge fund with a hedge fund manager. In this version of the analogy, NS is the hedge fund and NSH the hedge fund manager (i.e. hedge fund GP).

So to clarify what NS has done – they’ve invited in some new Limited Partners (think hedge fund investors) via their secondary offering of 12.5 million LP units raising $579MM (before fees). This money will, along with additional debt proceeds and cash, be invested in their $1.475MM purchase of Navigator Energy Services, owner of gathering and processing assets in the Permian Basin in West Texas. This looks just like a hedge fund leveraging new client capital to invest in assets, except that NS is buying physical assets rather than stocks, bonds or currencies like a hedge fund.

Like a hedge fund manager the GP, NSH, has directed all this activity while only providing their minor 2% GP share of the equity capital. NSH receives Incentive Distribution Rights (IDRs) from NS which are a function of NS’s Distributable Cash Flow (DCF). Since NS owns more assets, they’ll throw off more DCF which can only be good for NSH. So like any competent hedge fund manager, NSH will receive a portion of the cashflows generated by assets that it controls but does not finance.

We’ve written about this in the past (see Energy Transfer’s Kelcy Warren Thinks Like a Hedge Fund Manager)

NSH CEO William E. Greehey understands this profitable asymmetry better than most, because he personally owns 21% of NSH. He also regularly buys additional NSH units on the open market. The Hedge Fund Mirage; The Illusion of Big Money and How It’s Too Good To Be True (Wiley 2012) revealed that 98% of the profits generated by hedge funds had gone in fees to managers. Being a hedge fund client is often financially punitive and rarely anything like as lucrative as being a hedge fund manager. Although MLPs have easily outperformed hedge funds, it’s often still the case that GPs do better.

Greehey’s $250MM personal investment in NSH is augmented with $150MM in NS, so he is in a way invested alongside other NS holders. However, since the IDRs paid by his NS units are returning to him via his NSH ownership, he’s enjoying substantially better terms than the others. It’s like investing in a hedge fund for no fees, which given that industry’s history is usually the only sensible way to do so.

Of course, there’s always the risk that NS might have agreed to pay too much to acquire Navigator Energy Services, in the same way a hedge fund might invest its clients’ capital in a low-returning asset. The risk of overpaying is largely borne by NS (i.e. the hedge fund clients) since it’ll reduce the returns they’d otherwise earn. The impact on NSH is more muted – after all, they didn’t provide the capital in the first place so their downside is a bit less cashflow received on virtually nothing invested. NSH has agreed to waive its IDR payments on the new money for the first ten quarters, which helps the numbers in the short term but will still nonetheless provide accretive cashflows for the GP indefinitely thereafter.

Since investors are generally advised to place their capital alongside management, which in this case is clearly in NSH, one might ask what is driving the selection of investors who instead choose NS? But we won’t ask the question too loudly, because it is the existence of willing NS investors that creates value in NSH. After all, what use is a hedge fund manager with no hedge fund? Similarly, an MLP GP without a ready market for units in the MLP he controls is worthless. So NS holders will gamely look past the 7% drop in stock price on the day the secondary was announced and draw solace from the exciting prospects described by management on their explanatory conference call (although failing to allow questions made the exercise fairly pointless).

Hedge fund clients often warmly regard new investors as confirming their earlier insight, and pay little heed to the possibilty of a dilutive return on the additional capital raised. The more astute GPs chant “We Love Our LPs”, which is the mantra of every GP in finance. As holders of NSH, we love NS investors. Not so much that we’d want to be them of course, but they can feel the love and that’s what counts.

We are invested in NSH

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Leave a Reply

Want to join the discussion?Feel free to contribute!