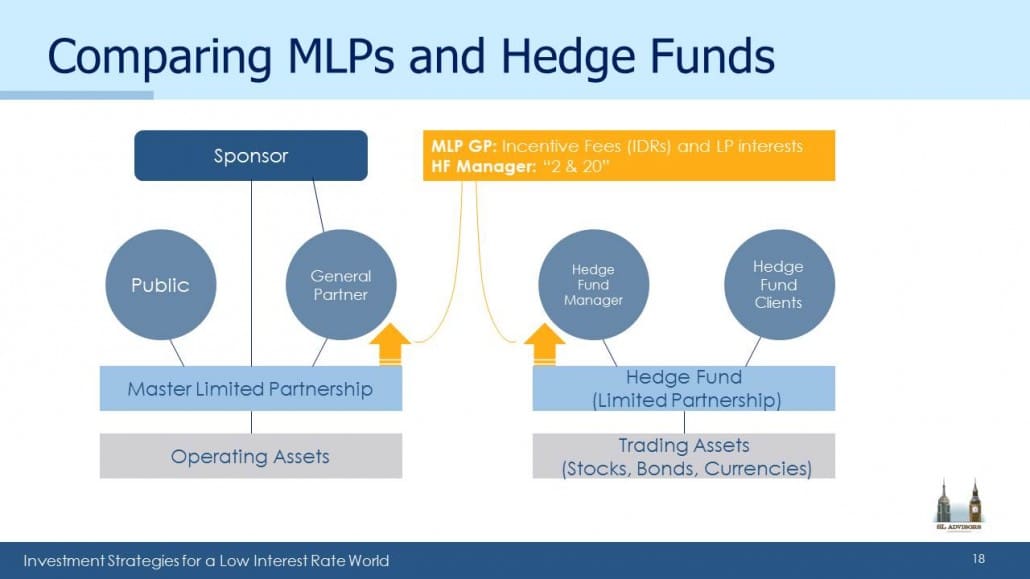

MLPs and Hedge Funds Are More Alike Than You Think

It usually pays to invest with management. In the hedge fund industry that has rarely been possible. Although most hedge fund managers invest in the fund they run, their wealth has come from owning the hedge fund General Partner (GP), which manages the fund. Opportunities to invest in hedge fund GPs are rare; they don’t need your capital and have little desire to share the lucrative economics.

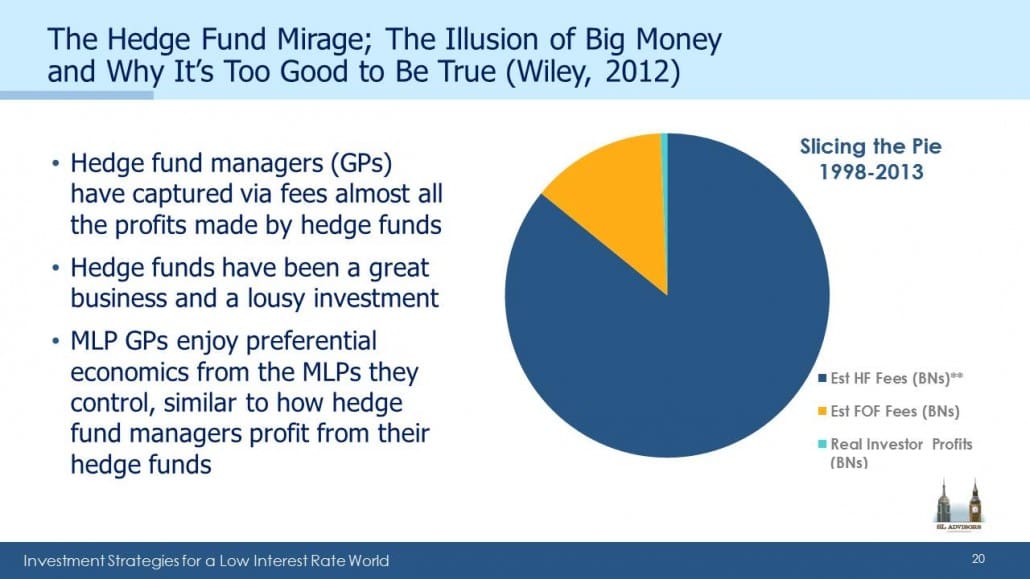

In 2012 I wrote The Hedge Fund Mirage; The Illusion of Big Money and Why It’s Too Good To Be True. The book pointed out what most hedge fund managers know – that hedge funds have been a great business and a lousy investment. Fees have eaten up virtually all the investment profits. Money still flows to hedge funds, because there are and always will be some good ones. But the farther you stray from a unique, specialized strategy the more prosaic your returns. The book drew some nice reviews and provoked few critics, because most industry insiders preferred to minimize awareness of the lopsided split of investment returns. Being controversial turned out to be great fun, and caused us to think differently about another asset class.

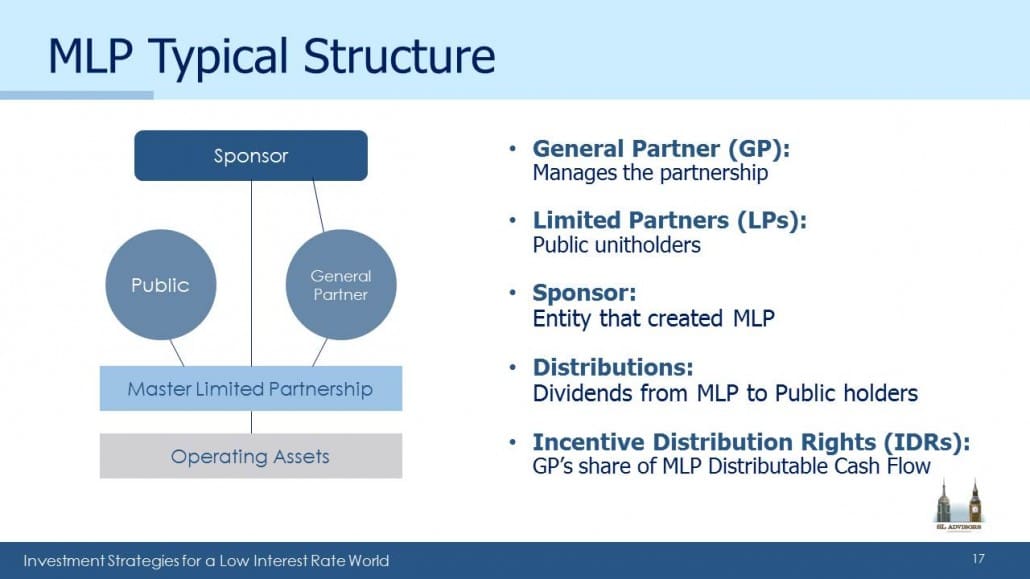

Master Limited Partnerships (MLPs) look like hedge funds. Although they own actual infrastructure assets rather than stocks, bonds and currencies, they share their organization as partnerships with hedge funds and private equity. MLP investors, like Private Equity (PE) fund investors, have limited rights. They’re called “Limiteds”, because Limited Partners (LPs) have little recourse once they’re invested (see The Limited Rights of Some MLP Investors).

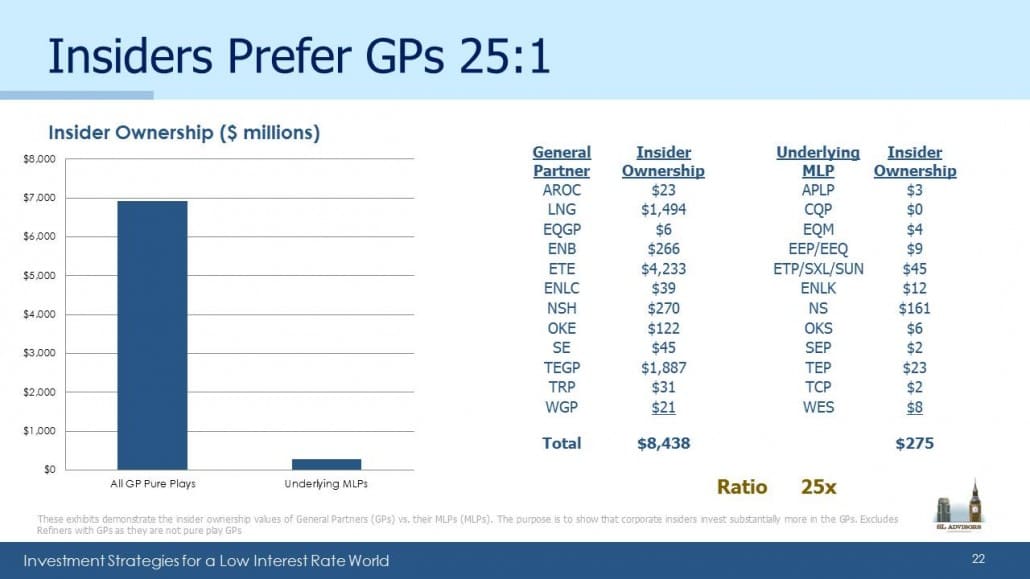

Not all MLPs have a GP, but many do and given how well hedge fund managers have done it’s no surprise that the people who run MLPs prefer to invest in the GP. The issue doesn’t receive much attention, but research we’ve done shows that in a select group of MLPs (i.e. those we care about) management has 25X as much money invested in GPs versus LPs.

Hedge funds and PE funds classically pay their GP “2 & 20”. This 2% management fee and 20% of the profits means, for example, that an 8% return after fees required a 12% return before fees. The 4% difference goes to the manager. MLPs pay their GPs Incentive Distribution Rights (IDRs), which direct a portion of the MLP’s Distributable Cash Flow (DCF) to the GP. The DCF split typically starts low but goes up to 50%, so the GP’s share can tend towards half.

The power of this becomes clear when you consider the financing of a new pipeline. GPs direct their MLPs to do something, the same way a PE manager directs his PE fund. A new pipeline is designed, planned, built and operated by an MLP on instructions from its GP, who then receives his share of the additional DCF created. Asset growth for PE managers is invariably beneficial, and it’s generally true as well for MLP GPs.

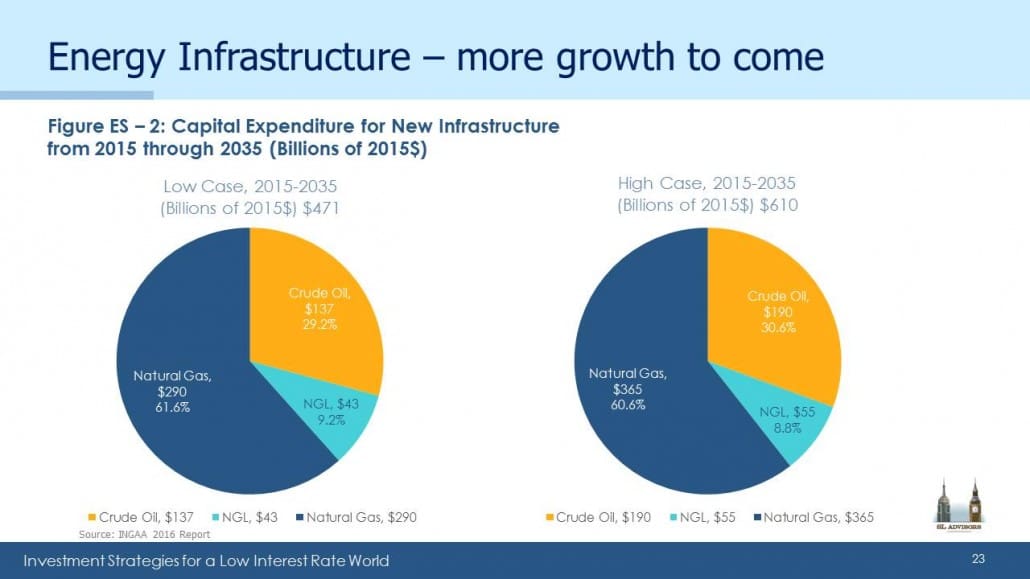

The best time to own hedge fund, PE or MLP GPs is during periods of asset growth. The Shale Revolution (see America Is Great!), with its growing output of crude oil, natural gas liquids and natural gas, is driving the need for more infrastructure assets. Recognition of this is behind the 25X statistic noted above.

It’s not a perfect analogy. For example, hedge fund investors have in aggregate done rather poorly, whereas 10 year MLP returns of 7.2% are better than REITs, Utilities and Bonds. Since MLP’s generally only raise equity from taxable U.S. investors tolerant of a K-1, they are limited to this relatively small portion of the global equity market. Those MLPs whose growth plans required several $BN have given up the lucrative GP/MLP structure in favor of being conventional corporations. But, as the 25X table shows, a decent number find the MLP structure still works.

At the MLPA Conference in Orlando a few weeks ago, questions usually concerned near term fluctuations in demand for one asset or another. We think the big trade here is America’s Path to Energy Independence, and owning GPs that benefit from continued infrastructure development. Conference chatter as well as attractive valuations show that it’s not yet a crowded trade.

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Leave a Reply

Want to join the discussion?Feel free to contribute!